What Is Whole Life Insurance? (& How To Get It)

By Les Masterson, Editor | Fact Checked Amy Danise, Editor

Jan. 31, 2024

Whole life insurance is one type of permanent life insurance that can provide lifelong coverage. It provides a variety of guarantees, which can be appealing to someone who doesn’t want any guesswork after buying life insurance.

Whole life insurance combines an investment account called “cash value” and an insurance product. As long as you pay the premiums, your beneficiaries can claim the policy’s death benefit when you pass away.

What Is Whole Life Insurance?

Whole life insurance offers coverage for the rest of your life and includes a cash value component that lets you tap into it while you’re alive.

Whole life insurance offers three kinds of guarantees:

- A guaranteed minimum rate of return on the cash value

- The promise that your premium payments won’t go up

A guaranteed death benefit amount

Whole life insurance is more expensive than term life insurance because people with a whole life policy are guaranteed to have a death benefit when they die. Term life insurance, on the other hand, offers level rates for a specific period, such as 20 or 30 years. Term life policies are cheaper than whole life insurance because they offer only coverage, not cash value.

Types of Whole Life Insurance

Participating vs. Non-Participating Whole Life

Policyholders of whole life insurance are usually eligible for annual dividends from the life insurance company. If you’re buying whole life insurance, confirm that the policy is “participating” so that you can reap the benefits of dividends.

- With a participating whole life insurance policy you are eligible to receive life insurance dividends from the insurer each year, which are essentially a refund of excess premiums paid by policyholders. Dividends are not guaranteed, but many life insurance companies are known for paying consistent dividends year after year. You can take the dividends in cash, use them to pay premiums, or use them to increase the face amount of your policy.

- With a non-participating policy you won’t get any dividends.

Whole Life Insurance Payment Types

You may find differences in how you can pay for a whole life insurance policy.

Pay premiums on a regular basis: You’ll pay a fixed amount monthly, quarterly, semi-annually or annually.

Single premium: You’ll pay the entire cost of the policy upfront. Cash value will be available right away and you’ll have no further premiums to pay.

Limited payment: You’ll pay regular premiums for a set number of years, such as 10 or 20 years. After this time period, the policy is paid up and no more payments are required.

Modified premium: Modified whole life insurance policies require premium payments that will increase after an introductory period. Your premiums will be lower for a set number of years—such as the first three to five—and then higher for the remainder of your lifetime. The death benefit will not change.

How Does Whole Life Insurance Work?

Whole life insurance works by first selecting the amount of coverage that best suits your needs. Once you have a policy, whole life insurance can remain in-force for your lifetime—as long as you continue to pay the premiums. Also, a cash value component will accrue over time.

Cash Value Accumulation in Whole Life Insurance

Whole life insurance is a type of cash value life insurance. Part of the premium payments for whole life insurance will accumulate in a cash value account, which grows over time and can be accessed with a policy loan, withdrawal or surrender of the policy.

Similar to a 401(k) or IRA, the money in the cash value account grows tax-free. However, if you take out cash value that includes investment gains, that portion will be taxable.

The accumulation of cash value is the major differentiator between whole life and term life insurance. While actual growth varies by policy, some take decades before the accumulated cash value exceeds the amount of premiums paid. This is because the entire premium does not go to the cash value—only a small portion. The rest goes to paying for the insurance itself and expense charges.

Most whole life policies have a guaranteed return rate at a low percentage, but it’s impossible to know how much your cash value will actually grow. That’s because most insurance companies that sell whole life also offer a “non-guaranteed” return rate of return based on dividends. You can choose to apply your dividends to cash value every year, but you can’t know how much that will amount to over time.

It may take decades for a policyholder’s cash value to exceed what’s paid in premiums.

Using the Cash Value in Whole Life Insurance

You can tap into cash value with a withdrawal or a loan, or also by surrendering the policy. If you take a loan, it’s tax-free, and you can pay it back, with interest. There are no taxes as long as your withdrawal is less than the portion of your cash value that’s attributable to premiums you’ve paid. If your withdrawal is greater, you’ll owe taxes on the difference because those are investment gains.

Outstanding loans and withdrawals will both reduce the amount of death benefit paid out if you pass away. That’s not necessarily a bad thing. After all, one of the reasons to buy a whole life insurance policy is to get cash value, so why let the money sit there without ever using it?

You want to be sure that you know all the ramifications of accessing cash value prior to making any decisions.

Death Benefit and Choosing Beneficiaries

When you buy a policy, you’ll choose a life insurance beneficiary to receive the death benefit. You don’t have to split the payout equally among beneficiaries. You can designate the percentage for each, such as 75% to Mary and 25% to John.

It’s also a good idea to designate one or more contingent beneficiaries. These folks are like your backup plan in case all the primary beneficiaries are deceased when you pass away.

Designating beneficiaries is an important task, as is keeping your designation up to date with your wishes. The life insurance company is contractually obligated to pay the beneficiaries named on the policy, regardless of what your will says. It’s wise to check once a year to verify your beneficiaries still reflect your wishes.

What Happens When You Die

A major selling point of whole life insurance is that it will be in force until your death, as long as you’ve paid the required premiums.

But here’s a kicker: For most policies, the policy pays out only the death benefit, no matter how much cash value you’ve accumulated. At your death, the cash value reverts to the insurance company. And remember that outstanding loans and past withdrawals from cash value will reduce the payout to your beneficiaries.

Some policies allow you to purchase a rider that gives your beneficiaries both the death benefit and the accumulated cash value. This provision also means you’ll pay higher annual premiums, as the insurance company is on the hook for a larger payout.

How Much Does Whole Life Insurance Cost?

While some of the cash value features and the permanent nature of whole life insurance sound appealing, whole life insurance is simply unaffordable for many people.

Many life insurance shoppers look at term life vs. whole insurance costs. It’s never an apples-to-apples comparison because the policies are so different. That said, here are examples of whole life insurance quotes based on a 30-year-old male of average height and weight for $500,000 in coverage.

This cost differential makes whole life insurance far less attractive to many individuals with an insurance need.

Here is a life insurance calculator to help you determine your life insurance needs.

Factors That Affect Whole Life Insurance Premiums

The coverage amount you choose will help determine your rate, along with:

- Age and gender

- Height and weight

- Past and current health conditions

- The health history of your parents and siblings

- Nicotine and marijuana use, including nicotine patches and gum

- Substance abuse

- Credit

- Criminal history

- Driving record (especially DUI convictions and moving violations, such as speeding tickets)

- Dangerous hobbies and activities (such as piloting planes or rock climbing)

With whole life insurance, there are a variety of other features and provisions that can affect costs as well, such as:

- Payment period: You can choose to pay for the entire policy in a short time frame, such as 10 or 20 years. The premium would rise substantially given the front loading of payments.

- Guaranteed return rate: Some companies offer a higher guaranteed return, which can result in higher annual premiums.

- Dividend crediting: Many whole life policies pay out a dividend, and policyholders can choose how to receive it. Receiving your dividend payments as a credit toward premiums reduces your annual out-of-pocket cost.

A Whole Life Insurance Example

Say you have purchased a whole life insurance policy with a death benefit of $500,000 and you’re paying $750 a month for it. You also get dividends every year. After 20 years, your cash value is $172,000. (Check your own policy illustration to see exactly how cash value will build in your own policy.) If you pass away at this time, your beneficiaries will receive $500,000. The $172,000 is absorbed back into the life insurance company.

Or let’s say you have the same policy but you took a $50,000 withdrawal of cash value, leaving $122,000 in cash value. If you pass away, your beneficiaries will receive $450,000 (the $500,000 death benefit minus your $50,000 withdrawal.) The $122,000 left in cash value is absorbed back into the insurance company.

Options for Surrendering Whole Life Insurance

With term life insurance, if you no longer have a need for insurance, you can simply stop paying. If you stop paying, the term life policy lapses and the insurance company will no longer pay a death benefit if you pass away.

Whole life insurance isn’t that simple. If you stop paying, the insurance company will use the cash value to pay any premiums until the cash value runs out and the policy lapses. But there are alternatives to simply stopping payments.

Options vary depending on your plan but can include the following tactics.

Take the Cash Surrender Value

To take the cash surrender value of a whole life insurance policy, simply tell the life insurance company that you want to take the cash and end the policy. You’ll receive the cash value minus any surrender charge. This action ends the insurance policy, so you should only do this if you no longer have a need for insurance, or you have new insurance in place.

If you take the cash surrender value, you’ll have to pay income taxes on any investment gains that were part of the cash value.

Ask About Reduced Paid-Up Life Insurance

A reduced paid-up life insurance policy may be an option. If you want a paid-up policy with a smaller death benefit, the life insurance company takes what you’ve already paid in, calculates how large of a death benefit that would provide, and gives you a policy with the lower death benefit amount. This avoids any taxes and leaves you with some life insurance still in place.

Extended Term Life Insurance

To do extended term life insurance, the life insurance company takes what you’ve already paid in and converts the whole life policy into a term life policy for the same death benefit. How long the term life policy lasts depends on how much you’ve paid, how old you are and the company’s current rates for a policy of that size and duration. This is helpful for someone who wants to preserve some life insurance for a short period of time, but no longer has a need for whole life insurance.

1035 Exchange

In a 1035 exchange, you can exchange your policy for a different life insurance policy or for an annuity. This can make sense to avoid taxes on the surrender value or if you realize another whole life policy has substantially better features and you’d prefer to have that policy instead.

Is Whole Life Insurance Worth It?

Given the expense of whole life insurance and that many people do not need insurance for their entire lives, whole life insurance is often not worth it.

However, there are some specific situations where buying another form of permanent life insurance makes sense. You might find that a universal life insurance policy is more affordable if lifelong coverage is your main goal.

Benefits of Whole Life Insurance

Permanent life insurance policies like whole life can be beneficial for long-range financial planning. Be sure to investigate other forms of permanent life, though, before you pay for a whole life policy.

- Provides lifelong coverage: As long as you keep up with premium payments, you’ll have peace of mind knowing that your beneficiaries will receive a life insurance payout.

- Dividends usually paid to you: Most whole life insurance policies have the potential to get annual dividends paid by the insurer.

- Cash value builds: A whole life insurance policy can accumulate a good amount of cash value over time. You can take advantage of the cash value through policy loans and/or withdrawals.

- Funding a trust: Permanent life insurance like whole life can be used to fund a trust that will support children after you die.

- Paying estate taxes: For those with estates larger than the current estate tax exemption, which is $12.92 million for an individual ($25.84 million per married couple) in 2023, permanent life insurance can make sense to help heirs pay estate taxes after you pass away. Some states have lower estate tax limits, so it may make sense for folks living in those states as well.

- Funding a buy-sell agreement: If you’re an owner of a business with a partner, you might need permanent life insurance to fund the purchase of each other’s shares in the business at death. Whole life insurance is one option for a buy-sell agreement.

Disadvantages of a Whole Life Insurance Policy

- Expensive: Whole life insurance policy tends to be an expensive way to buy coverage. Depending on your priorities, a different type of life insurance might be better. For example, if your main goal is to provide a death benefit to beneficiaries and you don’t care much about cash value, guaranteed universal life insurance can be a more cost-effective choice.

- Inflexible: You won’t have the ability to make adjustments to your premium payments and death benefit, which you would have with a universal life insurance policy.

- No benefit from good stock market years: The fixed-rate growth of cash value is something you might appreciate about a whole life insurance policy, but you’ll also be missing out on potential investment gains. The guaranteed cash value growth could be only 2% or 3%. Make sure to look at the policy illustration to see the projections of guaranteed cash value over time.

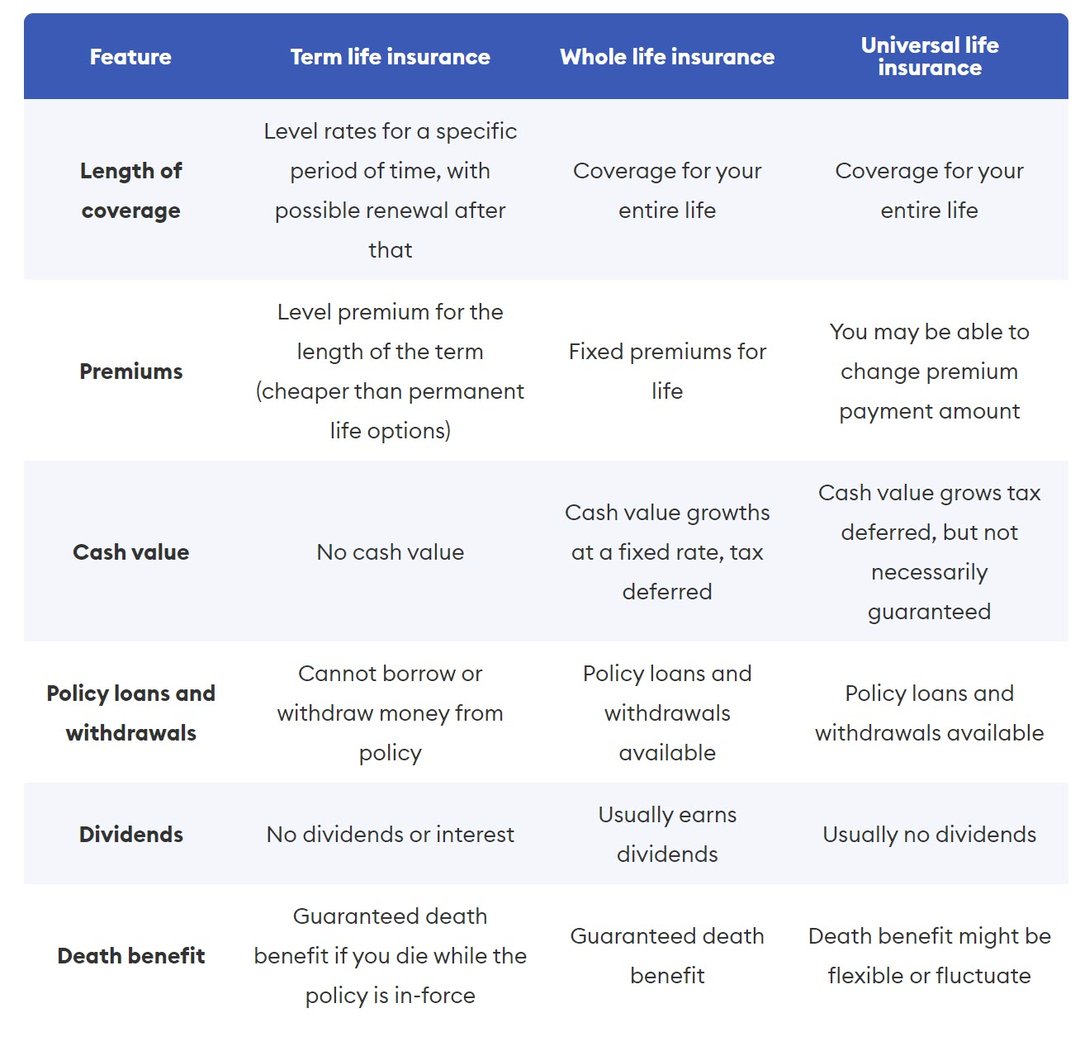

Whole Life vs. Term Life vs. Universal Insurance

The key differences among whole life, term life and universal life insurance are the length of coverage, the ability to build cash value and the flexibility of premiums and death benefit.

What is the difference among term life, whole life and universal life insurance?

Term life insurance is good for people who want a financial safety net for a specific number of working years, such as the years of paying off a mortgage. You lock in level premiums for the term length, such as 10, 15, 20 or 30 years. A small number of companies even offer 35-year and 40-year term life insurance. There’s no cash value.

Whole life insurance is good for people who want lifelong coverage, premiums that don’t change and a cash value component. Your beneficiary will get a life insurance payout no matter when you die, as long as you’ve paid the premiums needed to keep the policy in force.

Universal life insurance is another type of permanent life insurance. It might be a good fit if you want the ability to tap into the policy’s cash value and the flexibility to adjust premium payments and death benefits as your needs change.

© 2024 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.

The information in this communication or any information within the faoncall.com domain, and or any attachments to any Financial Advisor On Call communication is strictly confidential and intended solely for the attention and use of the named recipient(s). If you are not the intended recipient, or a person responsible for delivering this email to the intended recipient, please immediately destroy all copies of this email. Any distribution, use or copying of this e-mail or the information it contains by other than an intended recipient is unauthorized. This information must not be disclosed to any person without the permission of Financial Advisor On Call. Please be aware that internet communications are subject to the risk of data corruption and other transmission errors. For information of extraordinary sensitivity, we recommend that our clients use an encrypted method when they communicate with us.

*Financial planning and financial advisory services are offered by FAOC, LLC, a registered investment advisor (RIA). FAOC, LLC, is a wholly-owned subsidiary of Financial Advisor On Call, LLC, a fintech company offering educational services and record management support.