What Is the Lowest Mortgage Rate Ever?

Holly Johnson

June 25, 2024

While consumers have no control over mortgage rate trends, this factor plays a huge role in home affordability. The lowest average mortgage rates on record came about when the Federal Reserve lowered the federal funds rate in 2020 and 2021 in response to the pandemic. As a result, the average 30-year, fixed-rate mortgage fell to 2.65%, while the average 15-year, fixed-rate mortgage sunk to 2.10%.

KEY TAKEAWAYS

- The lowest average mortgage rate for 30-year, fixed-rate mortgages was 2.65% in January of 2021, whereas the lowest average rate for 15-year, fixed-rate home loans came in at 2.10% in July of 2021.

- These record-low mortgage rates resulted from the Federal Reserve’s changes to the federal funds rate due to the pandemic.

- Mortgage rates dramatically impact the costs of homeownership in either a positive or negative way. Where higher rates lead to more expensive mortgage payments, lower rates lead to lower payments.

- Shop around with mortgage lenders to find the best rates available today, and consider different types of home loans as well.

Understanding Mortgage Rates

The term “mortgage rate” refers to the rate at which you are charged to borrow money to purchase a home. There’s a difference between the interest rate on your mortgage and your loan’s annual percentage rate (APR). Where the interest rate is the rate at which you are charged interest, APR also reflects the fees you pay. These can include mortgage points and other charges.

Factors Influencing Mortgage Rates

Several factors can influence the mortgage rates you’re asked to pay when applying for a home loan. It all starts with the economic factors that impact mortgage rates on a national level in the first place, including changes to the federal funds rate initiated by the Federal Reserve.

Bond rates can also influence mortgage rates, as do a homebuyer’s individual financial factors when they apply for a loan.

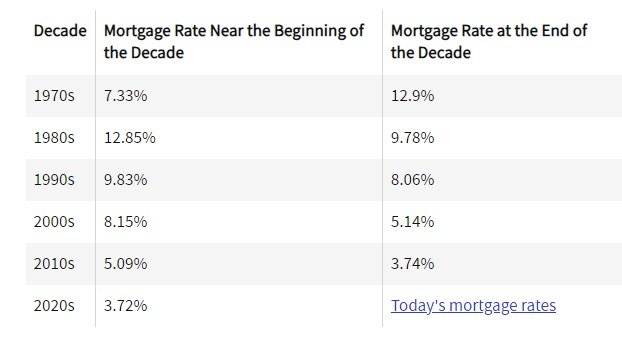

Historical Overview of Mortgage Rates

Mortgage rates ebb and flow over time based on the Fed’s reactions to various market conditions and movements within the overall economy. The chart below shows how mortgage rates changed from the 1970s to the 2020s.

The Lowest Mortgage Rate Ever Recorded

The lowest average mortgage rate for the 30-year, fixed-rate mortgage was recorded at 2.65% in January of 2021, whereas the lowest average rate for the 15-year, fixed-rate home loan came in at 2.10% in July of 2021. Keep in mind that these are the lowest average rates recorded and that some homeowners were able to secure lower interest rates during this time.

How Are Mortgage Rates Determined?

The Role of the Federal Reserve

While the Fed doesn’t directly influence mortgage rates, it does set the fed funds rate — the rate banks pay when they lend money to one another. This rate directly impacts various rates that borrowers pay, and the Fed is constantly updating its policies to reflect current market events and economic conditions.

According to the Fed, its policies have evolved quite a bit since the financial crisis of 2008. It established a near-zero target rate for the fed funds rate to help ease the worst impacts of the crisis at that time, then continued using monetary policy to suppress interest rates to support job creation and economic growth through 2014.

Interest rates remained relatively low through 2019 and 2020. The Fed lowered the fed funds rate considerably during this time in order to bolster the struggling economy and “smooth functioning of short-term U.S. dollar funding markets.” This move led to the lowest average mortgage interest rates ever recorded.

Note

The Fed repeatedly increased the fed funds rate in order to combat rising inflation throughout 2022 and 2023, which has led us to today’s average mortgage rate (as of June 20, 2024) of 6.87% for 15-year, fixed-rate mortgages and 6.13% for 30-year, fixed-rate loans.

The Impact of the Bond Market

The bond market, and especially the 10-year Treasury yield, also impacts mortgage rates. Generally speaking, bond and interest rates tend to move in the opposite direction. This means that increases in market rates typically correlate with bond prices falling, and vice versa.

Lender Considerations

Beyond external factors that are beyond a homebuyer’s control, personal factors also impact the interest rates they’ll see when applying for a mortgage. The following factors are at the top of mind of lenders each time you apply for a new home loan or refinance loan.

- Credit Score: Individuals with better credit can qualify for lower mortgage rates overall with many loan types.

- Down Payment: Larger down payments can help buyers secure a lower mortgage rate.

- Interest Rate Type: The choice between a fixed interest rate and an adjustable one can impact the rate you pay.

- Loan Amount: The price of a home and loan amount can also play a role in mortgage rates.

- Loan Term: Shorter-term home loans tend to come with lower interest rates than loans with longer repayment terms.

- Loan Type: The type of mortgage you apply for can impact your mortgage rate, whether you opt for a conventional mortgage, Federal Housing Administration (FHA) loan, U.S. Department of Agriculture (USDA) home loan, or VA loan.

- Location: Some regions of the country have higher or lower mortgage rates overall.

What Were the Highest Mortgage Rates in History?

According to Freddie Mac, mortgage rates peaked in October of 1981 when the average rate on 30-year, fixed-rate mortgages was 18.63%.

How Often Should You Compare Mortgage Rates?

Compare mortgage rates any time you plan to purchase or refinance a home. You may be able to find lower rates with some lenders than others if you shop around.

What Is the Trend in Mortgage Rates Since 2020?

Mortgage rates were already relatively low when the pandemic hit in 2020, but rates dropped even lower due to changes to the fed funds rate initiated by the Fed in 2020 and 2021. Mortgage rates have slowly been climbing ever since.

Can Mortgage Rates Ever Fall to Zero?

While the mortgage rates consumers pay will never fall to zero, the fed funds rate has been close to zero before. In fact, the federal funds rate dropped as low as 0.05% in April of 2020.

How Do Changes in Mortgage Rates Affect Refinancing?

Changes in mortgage rates impact the rate you’ll have to pay to refinance your mortgage. That’s why mortgage refinancing increases when rates drop and applications for mortgage refinancing decrease when rates are high.

The Bottom Line

Today’s mortgage rates aren’t as low as they were in the early 2020s, but they’re still relatively low when you look at historical averages. In fact, mortgage rates were higher from the 1970s to the 2000s before temporarily dropping and then leveling out where they are today.

Regardless, homebuyers have no control over the average mortgage rates. They only have control over the personal factors that apply when buying or refinancing a home, such as their credit score, down payment (for a home purchase), and the type of home loan they apply for. The best move most homeowners can make before taking out a mortgage is getting their own financial house in order, which may include raising their credit score and shopping around to find the best rates available.

The information in this communication or any information within the faoncall.com domain, and or any attachments to any Financial Advisor On Call communication is strictly confidential and intended solely for the attention and use of the named recipient(s). If you are not the intended recipient, or a person responsible for delivering this email to the intended recipient, please immediately destroy all copies of this email. Any distribution, use or copying of this e-mail or the information it contains by other than an intended recipient is unauthorized. This information must not be disclosed to any person without the permission of Financial Advisor On Call. Please be aware that internet communications are subject to the risk of data corruption and other transmission errors. For information of extraordinary sensitivity, we recommend that our clients use an encrypted method when they communicate with us.

*Financial planning and financial advisory services are offered by FAOC, LLC, a registered investment advisor (RIA). FAOC, LLC, is a wholly-owned subsidiary of Financial Advisor On Call, LLC, a fintech company offering educational services and record management support.